Figuring out who owes what when you are married can be a bit of a puzzle, can't it? It's a question many people ponder, especially when finances get a little tight or when thinking about the future. You might wonder, "In what states are you responsible for your spouse's debt?" This is a really important thing to understand, because the rules change quite a bit depending on where you live. It's not the same everywhere across the country, which is something you learn when you look at all the different state facts, you know, like how each state has its own bird or flower. Just like those unique symbols, each state also has its own approach to marital finances, and that truly makes a difference for couples.

For instance, some states see married couples as a single financial unit, sharing everything, while others consider each person's money matters to be pretty separate, even after saying "I do." This difference can really affect whether you might have to pay back money your spouse borrowed or spent. It's not always obvious, and sometimes people are surprised by what they discover about these laws. So, understanding these state-specific rules is a good idea for anyone tied together financially.

This article will help clear things up about marital debt responsibility across the United States. We'll look at the main types of states when it comes to shared debt and what that might mean for you. It's about knowing what to expect, and really, what your duties might be, so, you can plan accordingly. This information can help you protect yourself and your family's financial well-being.

- Does Kate Wear A Wig

- What Did Rose Mcgowan Share Her Biggest Regret About Shannen Doherty

- How Much Did Alyssa Milano Make Per Episode Of Charmed

- What Is Princess Kates Diagnosis

- Why Did Shannen Doherty Not Get Along With Alyssa Milano

Table of Contents

- Understanding Marital Debt Rules

- Community Property States and Debt

- Separate Property States and Debt

- Exceptions and Nuances to the Rules

- Protecting Yourself from Spousal Debt

- Frequently Asked Questions (FAQs)

Understanding Marital Debt Rules

When people get married, their lives often become very intertwined, and that includes their money matters. It's not just about sharing a home or a last name; it's about shared financial futures, you know? The rules about who is responsible for debt a spouse takes on can be quite different from one state to another. This is because each state has its own way of looking at property and debt that comes up during a marriage. It's a bit like how each of the 50 states has its own unique capital city or official song, as we see when we look at state information resources; their legal systems also have distinct features.

These state-specific approaches are generally grouped into two main types: community property states and separate property states. Each type has its own set of guidelines for how debts are handled when you are married. Knowing which category your state falls into is the first step in figuring out your potential responsibility. It's a fundamental difference that shapes how courts and creditors might view your financial ties. So, really, it's worth taking the time to understand this basic distinction.

Community Property States and Debt

In certain parts of the country, the law treats married couples as a single financial unit, which is a big deal for debt. This means that most property and debts acquired during the marriage are considered to belong equally to both spouses. It's a concept that has roots in older legal traditions, and it means that, you know, what one person takes on financially, the other might also be on the hook for.

- Do Shannen Doherty And Rose Mcgowan Get Along

- Where Does Julian Mcmahon Live

- What Were Queen Elizabeths Last Words

- What Is The Longest Someone Has Lived With Leukemia

- Why Did Alyssa Milano Fire Shannen Doherty

What Community Property Means

The idea of community property means that nearly everything a couple gains or owes from the wedding day forward is shared, 50/50. This includes things like earnings, houses bought together, and even credit card bills or loans taken out by one spouse during the marriage. It does not usually include things owned before the marriage or gifts and inheritances received by just one person. So, if your spouse gets a car loan while you are married, that debt could be seen as a shared responsibility, even if only their name is on the loan papers. This system aims to make sure both people have an equal stake in the financial life they build together, which is pretty fair in some respects.

Even if one spouse racks up debt without the other knowing, it could still be considered community debt if it was for the benefit of the marriage or family. For example, if a spouse takes out a loan for home repairs, that debt would likely be shared. This can be a surprising thing for some people to find out, as a matter of fact. It's a system that truly emphasizes the idea of a shared financial journey, for better or for worse, in a way.

States That Follow Community Property Rules

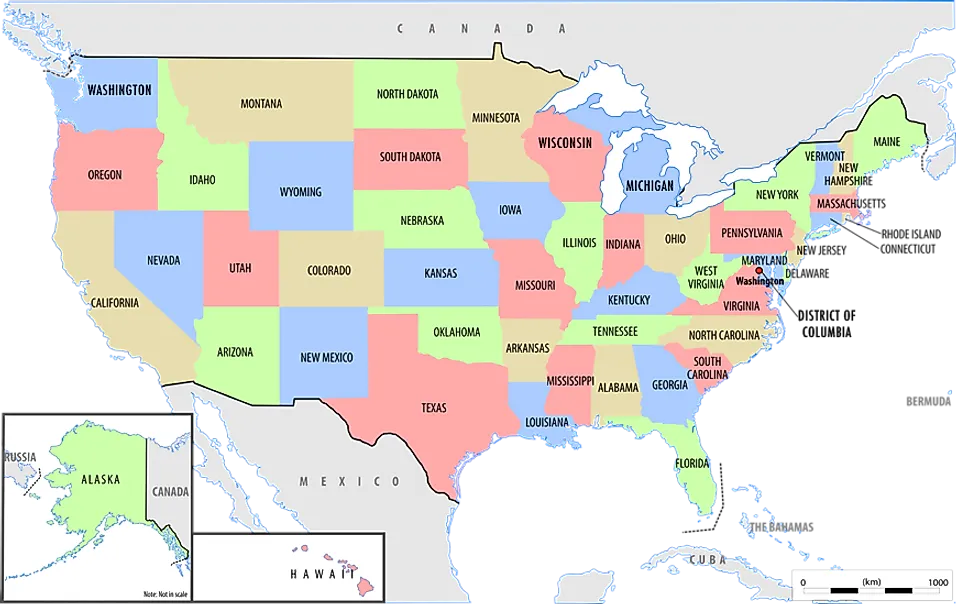

There are nine states that operate under community property laws. These are Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin. Also, Alaska allows couples to opt into a community property system through an agreement. Puerto Rico, a U.S. territory, also follows community property principles. So, if you live in one of these places, it's very important to be aware of these rules, because they affect your financial liability quite a bit.

For example, in California, a state known for its many regions and area codes, if one spouse takes out a loan for a new car during the marriage, that debt is generally considered community debt. This means both spouses are responsible for it, even if only one person signed the loan agreement. It's a key distinction that shapes how financial issues are handled, especially if a marriage ends. Knowing this can help you make more informed financial choices, you know, as a couple.

Separate Property States and Debt

Most states in the U.S. follow a separate property system, which is quite different from community property. In these states, what's yours is generally yours, and what's your spouse's is theirs, even after marriage. This approach means that, typically, each person is responsible for their own debts, unless they specifically agree to share them. It's a more individualistic view of finances within a marriage, actually.

How Separate Property States Handle Debt

In a separate property state, if your spouse takes out a loan or runs up a credit card bill in their own name, you are generally not responsible for that debt. This holds true even if they took on the debt during your marriage. The idea is that each spouse maintains their own financial identity and obligations. So, if your partner buys a new gadget on their credit card, that bill typically stays with them. It's a pretty straightforward idea, in some respects.

However, there are some important exceptions to this general rule. For instance, if you co-sign a loan with your spouse, then you are absolutely responsible for that debt, regardless of the state's property laws. Also, debts for "necessities" like food, shelter, or medical care can sometimes become shared responsibilities, even in separate property states. We'll get into those specific situations a little later. But, generally, the financial lines are drawn more clearly here, which can be a relief for some people.

States That Follow Separate Property Rules

All states not listed as community property states fall under the separate property category. This includes a vast majority of the U.S. states, from New York to Florida, and everywhere in between. This means that in places like Ohio or Georgia, if your spouse takes out a personal loan, that debt usually belongs solely to them. It's a common legal framework across most of the country, you know.

Understanding this distinction is really important, because it shapes how you might approach financial planning and joint purchases. It also affects how creditors can pursue debts. For instance, a creditor generally cannot come after your individual assets to pay off a debt that is solely in your spouse's name in a separate property state. This provides a certain level of protection for individual finances within a marriage, which is a good thing to be aware of, actually.

Exceptions and Nuances to the Rules

While states generally fall into either community property or separate property categories, the reality is a bit more complex. There are specific situations where debt responsibility can change, regardless of the state's main classification. It's never quite as simple as just one rule, is it?

Debts for Necessities

Even in separate property states, there's a legal concept called the "doctrine of necessaries" or "family expense laws." This means that both spouses can be held responsible for debts incurred for essential items or services for the family. This often includes things like food, housing, clothing, and medical care. So, if one spouse gets sick and racks up medical bills, the other spouse might still be on the hook for those costs, even if they didn't sign anything. This is because these are seen as basic needs for the family unit, you know.

This rule exists to ensure that families can get the things they need to survive, even if one spouse is unable or unwilling to pay. It's a safety net, in a way, but it also means a potential liability for the other spouse. This can be a surprising exception for many people who think their finances are entirely separate. So, it's something to definitely keep in mind, pretty much.

Jointly Held Debt

This is probably the most straightforward exception: if you co-sign a loan or open a joint credit card account with your spouse, you are both equally responsible for that debt. This is true in every state, whether it's community property or separate property. When you put your name on a loan alongside someone else, you are agreeing to pay it back if they don't. It's a direct agreement with the lender, after all.

This means that if your spouse stops making payments on a joint credit card, the creditor can come after you for the full amount owed. Your credit score will also be affected by any late payments or defaults on that joint account. So, before you agree to share any debt, it's really important to understand the full implications. It's a big commitment, you know, signing on the dotted line together.

Premarital Debt

Generally, debts incurred by one spouse before the marriage remain that spouse's individual responsibility. This holds true in both community property and separate property states. Your partner's old student loans or credit card bills from before you tied the knot typically stay with them. You are not automatically responsible for those. So, that's a bit of good news for many people, really.

However, there can be some gray areas. For instance, if marital funds are used to pay off premarital debt, or if the premarital debt somehow benefits the marriage, things can get a little complicated, you know? But as a general rule, what was owed before the marriage remains the individual's burden. It's a pretty common understanding across the board, usually.

Post-Divorce Debt

When a marriage ends, debt responsibility can become a major point of discussion. A divorce decree will typically outline how marital debts are divided between the former spouses. However, this division by the court does not always release a spouse from their obligation to the original creditor. For example, if a divorce decree says your ex-spouse is responsible for a joint car loan, but they don't pay, the lender can still come after you if your name is on the loan. The divorce decree only governs the relationship between you and your ex, not between you and the lender. This is a very important distinction, as a matter of fact.

It's crucial to understand that creditors are not bound by a divorce decree unless they were part of that legal process, which they almost never are. So, even after a divorce, if you have joint debts, you might still need to make sure those debts are paid, perhaps by refinancing them into one person's name or by selling the asset that secures the debt. It's a complex area that often requires careful planning, you know.

Protecting Yourself from Spousal Debt

Knowing the rules is the first step, but taking action to protect your finances is just as important. There are several things you can do to avoid being unexpectedly responsible for your spouse's debts. It's about being proactive and having open conversations about money, which is always a good idea in any relationship, right?

First, always be aware of any accounts opened in your name or jointly. Regularly check your credit report with all three major credit bureaus. You can get a free copy once a year from AnnualCreditReport.com. This helps you spot any unfamiliar debts or accounts that might have been opened without your knowledge. It's a simple step that can save a lot of trouble, you know, in the long run.

Second, think very carefully before co-signing any loans or opening joint credit accounts. While it might seem helpful at the time, it ties your financial future directly to your spouse's payment habits. If you do co-sign, make sure you understand the terms and are comfortable with the risk. It's a big step, so, really, consider it carefully.

Third, consider a prenuptial or postnuptial agreement. These legal documents can spell out how assets and debts will be handled during the marriage and in the event of a divorce or death. While it might feel unromantic to talk about money before or during marriage, these agreements can provide a lot of clarity and peace of mind for both people. They help set clear expectations, which is actually a very good thing for a relationship.

Finally, keep open lines of communication about finances with your spouse. Talk about income, expenses, debts, and financial goals regularly. Surprises about money can be a major source of stress in a marriage. By being transparent and working together on financial decisions, you can avoid many potential problems. This way, you're both on the same page, more or less, and can support each other.

Frequently Asked Questions (FAQs)

Here are some common questions people ask about being responsible for a spouse's debt.

Can a spouse be held responsible for debt incurred before marriage?

Generally, no, a spouse is not responsible for debt incurred by their partner before the marriage. That debt usually remains the individual's responsibility. So, your spouse's old credit card bills or student loans from before you got married typically stay with them, you know, as their own burden. This is true in most states, whether they are community property or separate property states. It's a pretty common rule, actually.

What happens to debt if one spouse passes away?

When a spouse passes away, their individual debts are usually paid from their estate first. If there isn't enough money in the estate, the debt may go unpaid. However, if you co-signed on a loan or if you live in a community property state where the debt was considered community debt, you might still be responsible for it. It really depends on the type of debt and the state laws. So, it's not always a clear-cut situation, you know.

Is a spouse responsible for their partner's credit card debt?

This depends a lot on the state you live in and how the credit card was used. In separate property states, if the credit card is only in your spouse's name, you are generally not responsible. But in community property states, credit card debt taken on during the marriage is often considered community debt, making both spouses responsible. If you were an authorized user or co-signed the card, then you are definitely responsible, regardless of the state. So, it's a bit complicated, you know, and depends on the specifics.

Understanding the rules about marital debt responsibility is a really important part of financial planning for any couple. As we've seen, the answer to "In what states are you responsible for your spouse's debt?" is not a simple one; it varies quite a bit depending on where you live and the nature of the debt. Just like knowing all the different state abbreviations or where each capital is on a map, understanding your state's specific laws on debt can help you make better financial decisions. It's always a good idea to seek advice from a legal or financial professional for specific situations, as laws can be complex and change over time. Learn more about state laws on our site, and link to this page for more financial guidance.

Related Resources:

Detail Author:

- Name : Dr. Trystan Davis III

- Username : sauer.abdul

- Email : gaston.braun@gmail.com

- Birthdate : 1988-12-18

- Address : 705 Gerhold Hills Patriciafort, IL 43753-9444

- Phone : +13147584192

- Company : Pouros, Corkery and Ledner

- Job : Architectural Drafter

- Bio : Hic quia officiis vitae voluptatum qui et rerum voluptatem. Consequuntur dignissimos laboriosam voluptas sapiente optio quia corrupti.

Socials

twitter:

- url : https://twitter.com/pwaters

- username : pwaters

- bio : Ut ut iure blanditiis non. Non cum aperiam sunt. Hic quod ut autem et occaecati unde consequatur.

- followers : 4458

- following : 1063

facebook:

- url : https://facebook.com/pwaters

- username : pwaters

- bio : Nostrum repudiandae cum soluta iure incidunt soluta consequatur.

- followers : 3665

- following : 2637

instagram:

- url : https://instagram.com/pwaters

- username : pwaters

- bio : Corrupti quas repellat mollitia at autem nulla. Occaecati maxime illum dicta ullam.

- followers : 6092

- following : 1118