Many people wonder if there comes a point in life when the annual tax chore simply disappears. It's a common thought, especially as folks get older and maybe their working days are behind them. You might imagine a magic age where the government just says, "You're all set, no more forms for you!" That idea, you know, is pretty appealing for a lot of us.

The truth, however, is a bit more nuanced than a simple birthday cut-off. There isn't, in fact, a specific age where everyone automatically stops needing to send in their tax papers. Instead, it really comes down to how much money you receive and where that money comes from during the year, which is something many people overlook.

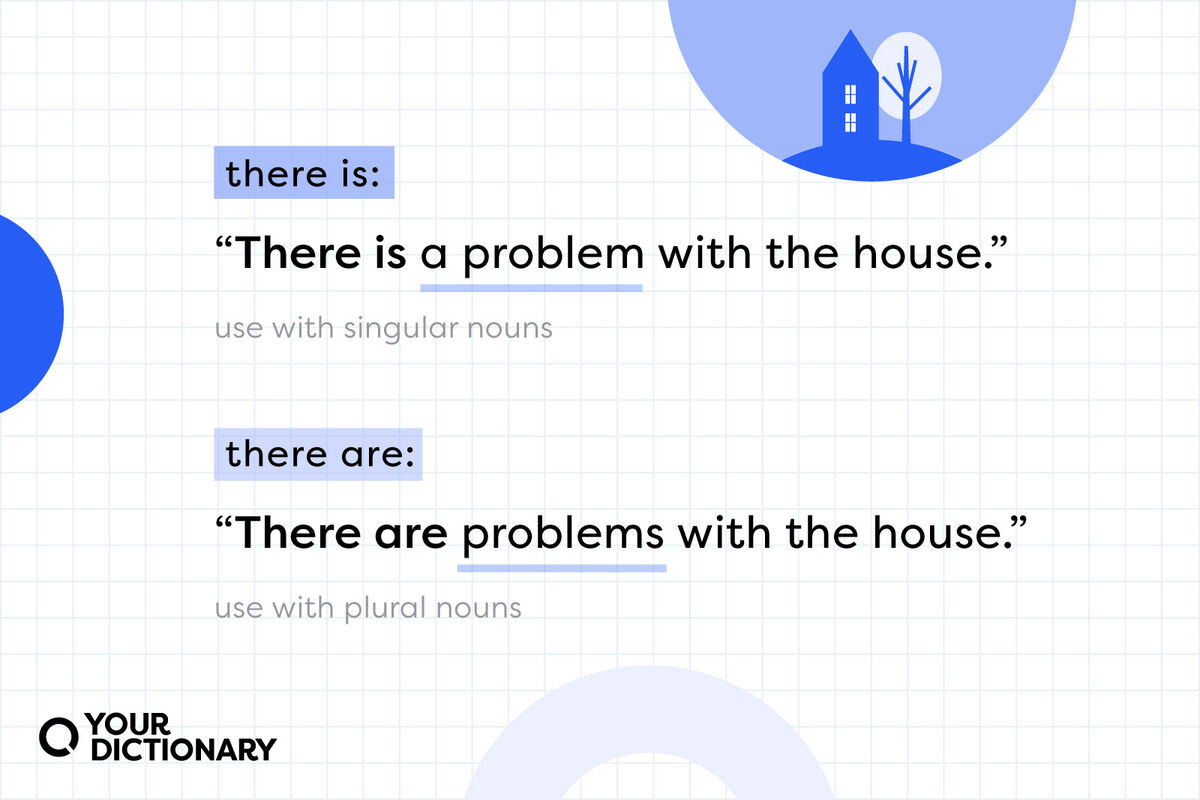

Figuring out tax rules can feel a little bit like trying to sort out confusing words, you know, like understanding the subtle differences between "there" and "their." As we've discussed in a previous article about common word usage, clear explanations make a big difference, and the same goes for tax requirements. It's all about getting the right information in the right place, basically.

- What Wrestler Had The Most Surgeries

- How Old Was Alyssa Milano When She Had Her First Child

- What Were Queen Elizabeths Last Words

- What Dress Size Is Kate Middleton

- Did Tori Spelling Date Anyone From 90210

Table of Contents

- The Core Idea: It's About Income, Not Just Years

- What Counts as Income for Tax Purposes?

- When You Might Still Need to File, Even If You Think Not

- Common Questions About Senior Tax Filing

- Getting Help and Staying Informed

The Core Idea: It's About Income, Not Just Years

The big thing to remember is that tax filing rules mostly depend on your total income for the year. It's not about how many birthdays you've had, but rather about how much money came in. So, a person who is 80 might still need to file, while someone who is 65 might not, depending on their earnings, you know.

This idea applies to everyone, really, no matter their age. The government sets certain income levels. If your income goes above these levels, then you generally have to send in a tax return. It's a pretty straightforward system in that regard, at least at its core.

Standard Deduction and Filing Thresholds

Each year, the tax rules include something called a "standard deduction." This is a set amount of money that reduces your taxable income. You can choose to take this standard amount or list out all your specific deductions, which is called itemizing. For many people, the standard deduction is simpler, and it's quite common, actually.

- Why Did Julian Mcmahon Leave Fbi Most Wanted

- Did Luke Perry And Shannen Doherty Get Along In Real Life

- What Color Does Kate Middleton Refuse To Wear

- Is Alyssa Milano A Democrat

- What Has Happened To Julian Mcmahon

For older people, the standard deduction is often a bit higher. This is a small benefit for those who are 65 or older, or if they are considered blind. It means they can earn a little more before they even have to think about filing. This extra amount helps, in a way, to reduce their tax burden.

The filing threshold is the income level where you must file a tax return. This threshold changes each year and depends on your filing status. Your filing status could be single, married filing jointly, or head of household, for example. These numbers are updated annually, so checking the current figures is always a good idea.

If your gross income, which is your total income before any deductions, is less than the standard deduction for your age and filing status, you might not need to file. This is a key point for many seniors. It’s a good rule of thumb, but there are exceptions, too, it's almost.

Special Rules for Older Folks

As mentioned, those who are 65 or older get a slightly larger standard deduction. This means they can earn a bit more money before they hit the filing requirement. It's a small nod to the unique financial situations that can come with age, in some respects.

There are also certain credits or deductions that might apply specifically to older adults. These can further reduce a person's tax bill or even eliminate it entirely. Knowing about these can save you money, or at least help you understand your situation better, you know.

For instance, some states offer property tax breaks for seniors. While these aren't federal income tax rules, they show how different parts of the tax system can help older people. It’s worth looking into all options, naturally.

What Counts as Income for Tax Purposes?

When we talk about income for tax purposes, it's not just about a paycheck from a job. It includes money from many sources. Knowing what counts is really important for figuring out if you need to file. It's more than just wages, you see.

Things like money from investments, pensions, and even parts of your Social Security can be considered income. Each type of income has its own set of rules, which can make things a little bit complicated. But understanding these different types helps, basically.

Social Security Benefits

For many older adults, Social Security benefits are a main source of money. A common question is whether these benefits are taxed. The answer is, well, sometimes, it depends on your other income, you know.

If Social Security is your only income, you generally won't have to file a tax return. This is because the amounts are usually below the filing thresholds. So, for many, this is good news, honestly.

However, if you have other income besides Social Security, such as a pension, wages, or interest, then a portion of your Social Security benefits might become taxable. This happens if your "combined income" goes above certain levels. Combined income is a specific calculation that includes half of your Social Security benefits plus your other income, you see.

Up to 85% of your Social Security benefits could be taxed if your combined income is high enough. This is a key detail that surprises some people. It’s important to calculate this carefully, or get help, of course.

Pensions and Retirement Accounts

Money you get from a pension or from traditional retirement accounts, like a 401(k) or a traditional IRA, is usually taxable when you take it out. This income adds to your total for the year. So, it definitely plays a role in whether you need to file, or not.

Roth IRA withdrawals, on the other hand, are typically tax-free if you meet certain conditions. This is a big difference and can affect your overall tax picture. Knowing the type of account you have matters, really.

If you are receiving regular payments from a pension, those amounts will add up over the year. They are counted as ordinary income. This can quickly push your total income above the filing threshold, you know.

Similarly, money taken from a traditional IRA or 401(k) is taxed as regular income. The amount you withdraw can make a big difference in your filing requirement. It's something to plan for, you see, especially if you take out a lot.

Other Income Streams

Interest from savings accounts or investments also counts as income. Dividends from stocks are another common type. These small amounts can add up, and they are definitely part of your overall income for tax purposes. They can push you over the edge, as a matter of fact.

Rental income from a property you own is also taxable. If you have a side gig or do some freelance work, those earnings are also counted. Basically, most money you receive, unless specifically exempted, is considered income. This includes things like capital gains from selling assets, too.

Even if you have very little of each type of income, when you put them all together, they might reach the filing threshold. This is why it's good to keep track of all your money sources throughout the year. It helps you avoid surprises, you know.

When You Might Still Need to File, Even If You Think Not

Sometimes, even if your income is below the filing threshold, it can still be a good idea to file a tax return. There are specific situations where filing could actually put money back in your pocket. It's not always about owing money, you see.

Many people miss out on refunds because they assume they don't need to file. This is a common mistake. It's worth checking, honestly, just in case.

Claiming a Refund

If you had taxes withheld from your pension or other payments during the year, you might be due a refund. This happens if too much tax was taken out. The only way to get that money back is to file a tax return. It's your way of asking for your money back, essentially.

Similarly, if you made estimated tax payments throughout the year, but your actual tax bill turns out to be lower, you'll need to file to get the overpayment back. This is pretty common for people with various income sources. It's like balancing your checkbook, really.

So, even if your income is below the amount that requires you to file, sending in a return could mean a nice check coming your way. It's definitely something to consider. Don't leave money on the table, you know.

Self-Employment Earnings

If you earn money from being self-employed, even a small amount, you might have to file. This is because there are special rules for self-employment tax. This tax helps cover Social Security and Medicare contributions. It's a different kind of tax, basically.

For the current tax year, if you have net earnings from self-employment of $400 or more, you generally have to file a tax return. This threshold is quite low, so it can catch people off guard. It's a very specific rule, you see.

This applies even if your total income from all sources is below the standard filing threshold. So, a small side job could mean you still need to file. It's important to keep track of these earnings, naturally.

Certain Tax Credits

Some tax credits are refundable. This means that if the credit amount is more than the tax you owe, you can get the difference back as a refund. You have to file a return to claim these credits. They can be a real benefit, you know.

Examples might include the Earned Income Tax Credit, though this is less common for retirees. However, there could be other credits related to education or certain types of expenses that might apply. It's worth exploring what's available, honestly.

Even if you don't owe any tax, claiming a refundable credit could result in a payment to you. This is a powerful reason to file, even when you think you don't have to. It's like finding extra money, pretty much.

Common Questions About Senior Tax Filing

People often have very similar questions about taxes as they get older. These are some of the most asked questions, you know, that come up quite a bit.

Do I need to file taxes if Social Security is my only income?

Generally, no, you usually do not need to file if Social Security is your only source of money. This is because the amount of Social Security benefits alone is typically below the income thresholds that require filing. It's a simple answer for many people, basically.

However, if you have other income in addition to Social Security, then a portion of your Social Security benefits could become taxable. This means you might then need to file. So, it's not always a straight "no," you see.

What is the income threshold for seniors to file taxes?

The income threshold for seniors to file taxes depends on their filing status and their age (65 or older, and if they are blind). These amounts change each year. For example, for a single person who is 65 or older, the threshold is higher than for someone under 65. You can find the exact numbers on the IRS website for the current tax year. It's really important to check the official figures, honestly.

It's your gross income that counts towards this threshold. That means all your money before any deductions. So, you need to add up everything to see where you stand, naturally.

Are there any tax breaks for older adults?

Yes, there are some tax breaks for older adults. The main one is the increased standard deduction for those aged 65 or older. This means they can deduct a larger amount from their income, which reduces their taxable income. It's a pretty good benefit, you know.

Also, some states offer property tax relief or other benefits for seniors. While not federal income tax breaks, these can still save money. It's worth looking into what's available where you live, you see.

There might also be a credit for the elderly or the disabled, which can help reduce tax liability for those who qualify. Eligibility for this credit can be a bit specific, so checking the rules is a good idea. It's another potential help, apparently.

Getting Help and Staying Informed

Tax rules can feel complex, even with all the clear explanations. It's perfectly fine to seek help. Many resources are available to make the process easier. You don't have to go it alone, you know.

Staying updated is also key. Tax laws can change, sometimes every year. So, what was true last year might be slightly different this year. It's a good habit to keep an eye on official announcements, naturally.

Resources for Seniors

The IRS offers free tax help programs, like the Tax Counseling for the Elderly (TCE) program. This program provides free tax assistance to people who are 60 or older. Volunteers are often retired individuals themselves, which is nice, you know.

Another option is the Volunteer Income Tax Assistance (VITA) program. While it serves a broader group, many seniors can also get help there. These services are really helpful for many people. Learn more about free tax help options on the official IRS site.

Local community centers or senior centers sometimes offer tax help sessions, too. These can be a great way to get personalized guidance. It's worth checking what's available in your area, basically.

Why Professional Advice Can Be a Good Idea

For more complex situations, or if you just want peace of mind, getting help from a tax professional can be very valuable. They can help you understand all the rules that apply to your specific situation. They know all the ins and outs, you know.

A professional can make sure you claim all the deductions and credits you are eligible for. This could save you money or prevent mistakes. It's an investment that often pays off, honestly.

They can also help with planning for future years, especially if your income sources might change. This kind of forward thinking is really helpful for managing your money. It gives you a clear picture, you see. Learn more about planning for retirement finances on our site, and link to this page for more tax tips for retirees.

Related Resources:

Detail Author:

- Name : Jerrod Kub

- Username : cortney58

- Email : alangworth@hotmail.com

- Birthdate : 1982-09-08

- Address : 57681 Matilda Ways Kossburgh, KY 50842-7422

- Phone : 321.976.2383

- Company : Wolff Group

- Job : Auditor

- Bio : Quia voluptatem esse delectus libero ullam. Aut ullam eum repellat omnis qui maiores. In iusto amet deleniti reiciendis possimus sunt.

Socials

linkedin:

- url : https://linkedin.com/in/idellwill

- username : idellwill

- bio : Earum quibusdam asperiores velit vel.

- followers : 4080

- following : 2148

instagram:

- url : https://instagram.com/idell8071

- username : idell8071

- bio : Temporibus perferendis voluptatem et vel. Alias sit veniam rerum provident dolores rem.

- followers : 1011

- following : 2907

facebook:

- url : https://facebook.com/idell.will

- username : idell.will

- bio : Id iure omnis eaque placeat illo id. Harum occaecati quis omnis qui tempora.

- followers : 5279

- following : 1257